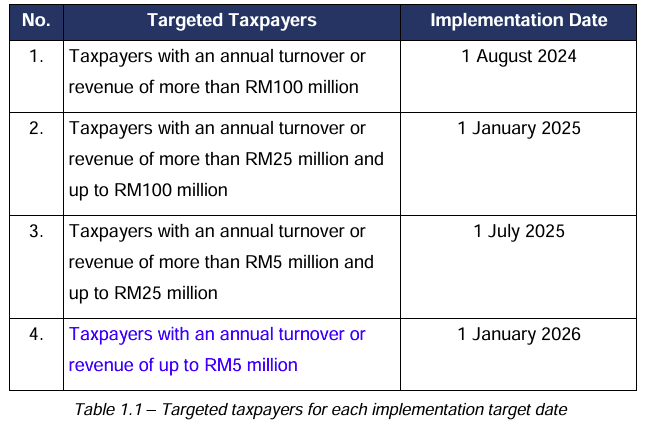

Due to the latest announcement, the last phase of e-Invoice implementation will be as follows:

The annual turnover or revenue for the implementation of e-Invoice will be determined based on the following:

1. Taxpayers with audited financial statements: Based on annual turnover or revenue stated in the statement of comprehensive income in the audited financial statements for financial year 2022.

2. Taxpayers without audited financial statements: Based on annual revenue reported in the tax return for year of assessment 2022.

3. In the event of a change of accounting year end for financial year 2022, the taxpayer’s turnover or revenue will be pro-rated to a 12-month period for purposes of determining the e-Invoice implementation date.

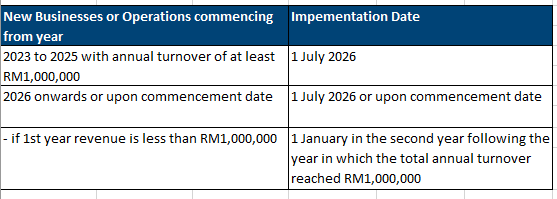

For new businesses or operations commencing from the year 2023 to 2025 with an annual turnover or revenue of at least RM1,000,000, the e-Invoice implementation date is 1 July 2026.

For new businesses or operations commencing from year 2026 onwards, the e-Invoice implementation date is 1 July 2026 or upon the operation commencement date. However, if the first year’s turnover or revenue is less than RM1,000,000, the e-Invoice implementation date would be 1 January in the second year following the year in which the total annual turnover or revenue reached RM1,000,000.

Exemption From Implementing e-Invoice

For the purposes of e-Invoice, the following persons are currently exempted from issuing e-Invoice (including issuance of self-billed e-Invoice):

(a) Foreign diplomatic office

(b) Individual who is not conducting business

(c) Statutory body, statutory authority and local authority, in relation to the following:

- collection of payment, fee, charge, statutory levy, summon, compound and penalty by it in carrying out functions assigned to it under any written law; and

- transaction of goods sold and services performed before 1 July 2025

(d) International organisation for transaction of any goods sold or service performed before 1 July 2025

(e) Taxpayers with an annual turnover or revenue of less than RM1,000,000.

However, based on the Frequent Ask Question (FAQ) issued by Inland Revenue Board of Malaysia on 9 July 2025, this exemption does not apply to the following taxpayers:

a) taxpayer with non-individual shareholder(s) (or equivalent) with annual turnover or revenue of at least RM500,000 RM1,000,000; or

b) taxpayer is a subsidiary of a holding company with annual turnover or revenue of at least RM500,000 RM1,000,000; or

c) taxpayer has related company* / joint venture with annual turnover or revenue of at least RM500,000 RM1,000,000.

*A “related company” has the meaning assigned to it in section 2 of the Promotion of Investments Act 1986.

Definition of related company is defined as:

(a) the operations of which are or can be controlled, either directly or indirectly, by the first-mentioned company;

(b) which controls or can control, either directly or indirectly, the operations of the first-mentioned company; or

(c) the operations of which are or can be controlled, either directly or indirectly, by a person who control or can control, either directly or indirectly, the operations of the first-mentioned company:

Provided that a company shall be deemed to be a related company of another company if—

- at least twenty percent of its issued share capital is beneficially owned, either directly or indirectly, by that other company; or

- at least twenty percent of its issued share capital of that other company is beneficially owned, either directly or indirectly, by the first mentioned company;

发表回复